Although risky and oftentimes complicated, the benefits of an acquisition can be significant. Rarely do middle-market companies have excess cash available to fund an acquisition. Financing the acquisition may be top of mind long before a transaction occurs; yet, many companies elect to put this step on hold until after the letter of intent has been negotiated. There are no templates for the ideal capital structure, and the range of advice related to financing alternatives, structure, and providers can be overwhelming.

Acquisition Financing: The process of paying for an acquisition target over time with the use of third-party debt and/or equity capital. The optimal capital structure carefully balances the cost of capital with the needs of the enterprise and the inherent risks affiliated with a transaction.

Acquisition financing in the middle market is available from many different types of lenders and investors. The thoughtful financier finds the right balance between maximizing return on equity and maintaining short and medium-term flexibility should an unforeseen need arise.

Not all Capital is Created Equal

A range of variables can influence the optimal capital structure for an acquisition. Industry trends, growth rate, the buyer’s existing balance sheet, integration considerations, margin stability, and forecasting scenarios can all contribute to selecting capital sources that are tailored to the buyer’s current and ongoing financial needs. Regardless of shareholder preference, lenders will also have strong beliefs regarding the balance of debt and equity that may be required to fund the proposed acquisition.

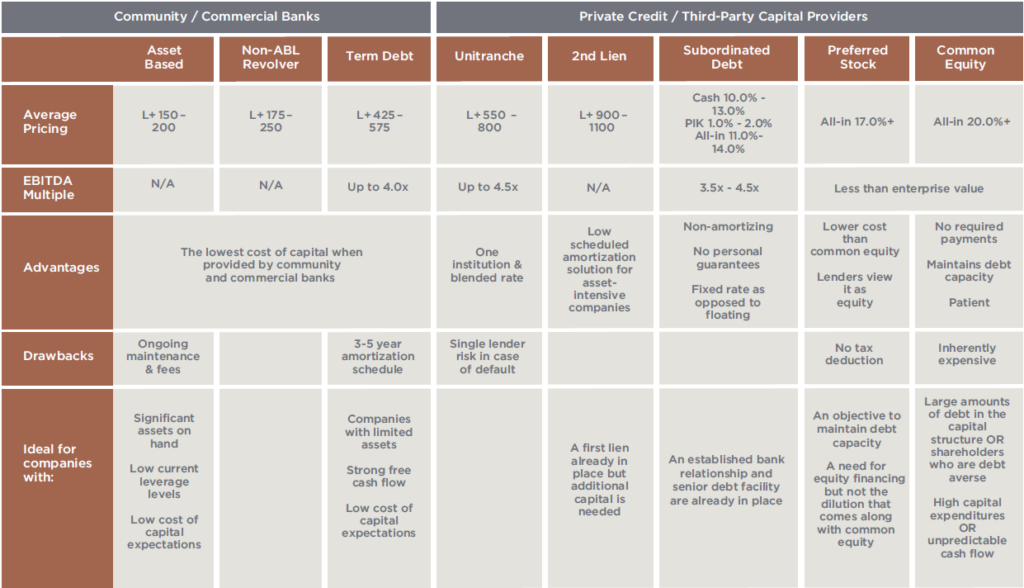

Lenders, like companies, are varied and include community banks, commercial banks, and a host of non-bank lenders, the latter of which are categorically referred to as private credit. Chartered banks, namely community and commercial banks, are oftentimes criticized for being too conservative with respect to how much leverage they are willing to provide; however, this is a direct result of restrictions placed on these institutions by various federal regulators seeking to protect the deposit accounts that represent the principal funding source for these banks. These de minimis interest bearing accounts are a low cost of funding, so while banks are extending less credit and taking less risk, relative to their non-bank counterparts, this lower cost of funds allows banks to charge lower rates. As a result, these institutions will likely offer some of the most competitive pricing and should be the first consideration for raising cost-effective capital.

For an owner or management team that is looking to raise more capital than a community or commercial bank can offer, private credit funds may be a stand-alone substitution or compliment to an existing or lower-cost bank solution. Private credit includes specialty finance companies, publicly traded business development corporations (BDCs), private credit funds, and mezzanine funds, among others. Because non-bank lenders rarely have deposit accounts or access to the Federal Reserve discount window, these institutions have a higher cost of funding. Private credit funds raise equity from investors, which may be leveraged. As a result, these credit funds must charge a higher interest rate than banks in order to satisfy a return their investors find commensurate with the risk, which is meaningfully higher than the return on interest-bearing FDIC insured deposits. While the interest rate is higher on private credit loans, most non-bank lenders will attempt to justify the increased cost of capital with higher advance rates, relaxed covenants, and lower amortization rates. Non-bank lenders may also have a willingness to extend credit to companies that may be considered a higher credit risk by the banks.

Moving beyond the lender orientation of commercial banks and private credit funds, many junior capital and equity funds categorically evaluate new opportunities using fundamental analysis and an investor’s mindset, a subtle yet important distinction. Owners and management teams need to ask themselves whether they want a lender that is often solely interested in protecting its principal or an investor who will work alongside a management team to mitigate unforeseen economic events and strategically address market opportunities in order to create long term economic value.

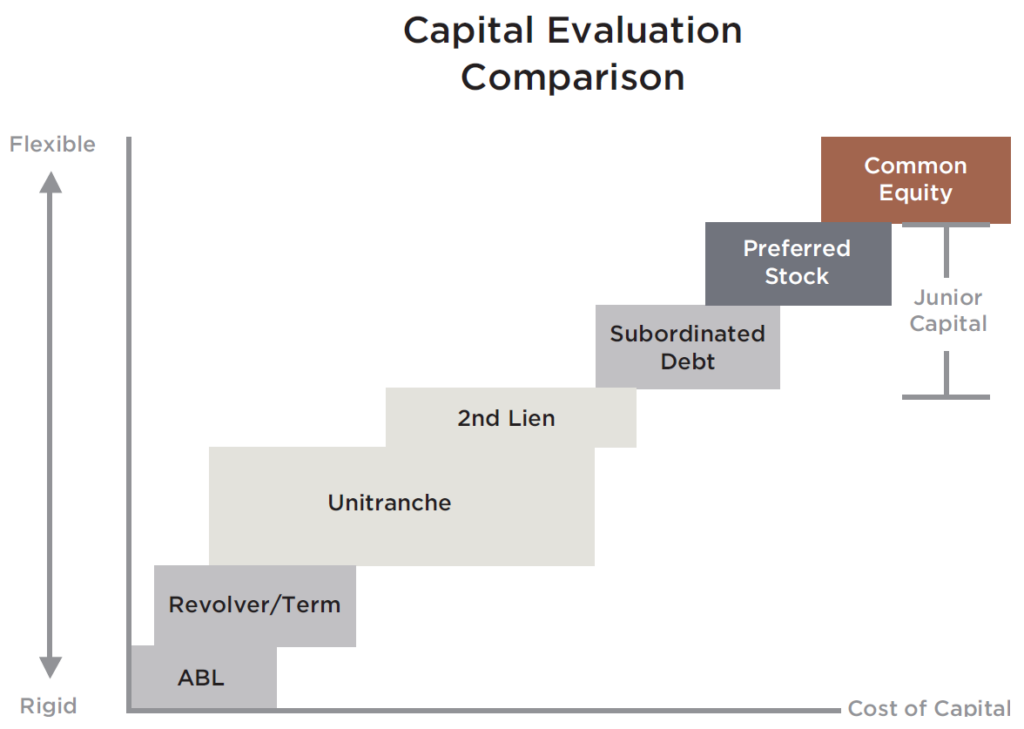

Capital Evaluation Comparison

When considering funding from bank and non-bank sources, the borrower, often referred to as the issuer, should generally measure the balance between cost and flexibility. The following comparison of securities offered by bank and non-bank providers indicates the correlation of cost (x-axis) and flexibility (y-axis) inherent to the terms of those securities (see Capital Evaluation Comparison chart on page 3). At one end of the spectrum, asset-based loans are generally very structured with set advanced rates against defined collateral and rigid covenants. With this collateralized position and the ability to monitor a loan, ABL providers can offer the lowest cost of capital. At the other end of the spectrum, equity securities generally do not include any financial covenants, set interest or dividend rates, or maturity dates representing greater financial flexibility under which the issuer can operate. However, an investor in these securities will expect the highest returns for giving up contractual recourse while patiently waiting for a sale of the company or buyout of their shares.

Although providers, interest rates, and leverage multiples may fluctuate with economic cycles, the aforementioned debt and equity securities provided by bank and non-bank lenders and investors are nuanced and offer a range of features as outlined below:

Senior Debt

As the name implies, senior debt sits at the top of the capital structure and remains first in priority of a borrower’s obligations. This form of capital was historically synonymous with large commercial banks; however, specialty finance companies also offer senior debt solutions. The rate differential between bank and non-bank senior debt loans can vary 200-900 basis points (bps). Senior debt providers will normally lend using one of two instruments. Asset-based loans (ABL) are secured by a company’s assets, which typically include anything that can be easily liquidated or recovered, including accounts receivable, equipment, machinery, inventory, real estate, and in some cases, intellectual property. An ABL may be structured as a term loan, but commonly it is structured as a Revolving Line of Credit, which is drawn subject to availability and the working capital needs of the business. Senior ABL structures are underwritten by considering the net orderly liquidation value (NOLV) of the company’s assets in the event of default or foreclosure. Upon signing a term sheet with an ABL provider, the lender will engage a third-party to appraise the company’s assets. These results will then factor into the lender’s final determination of whether the NOLV of the assets will cover the principal amount of the loan in the event of default. Accordingly, the asset-based lender will extend loans at a discount to the underlying collateral base, typically 80-85% against receivables and 50-75% against inventory and fixed assets.

While the interest rate on ABL structures from regulated banks is currently one of the lowest available, there are ongoing fees with these types of facilities, namely asset appraisals and collateral monitoring fees. For companies with significant collateral but unpredictable year-to-year performance, ABL may be more readily available from non-bank lenders who will charge high single digit and low double-digit interest rates.

Asset-based loans are a cost-effective alternative for companies that:

Operate in asset intensive industries (distribution, manufacturing, trucking, construction, metals recycling, equipment rental, used aircraft parts resale, etc.);

Don’t qualify for an enterprise value loan as they are prone to economic cycles or commodity fluctuations; and/or

Have collateral value that exceeds 50% of enterprise value.

For those asset-light companies that are looking for inexpensive bank debt, the regulated banks also offer revolvers and term loan solutions without the monitoring requirements of an ABL structure. These term loans carry a nominally higher interest rate, but the cost of capital is still well below the rates charged by non-bank lenders. While many community banks will look at the underlying collateral base as a proxy for lending limits, commercial banks will take the company’s enterprise value into consideration in addition to perceived cash flow coverage.

For example, a commercial bank believes that a $10 million EBITDA company’s enterprise value is $70 million. The commercial bank may be willing to lend up to $30 million via $8 million drawn against inventory and receivables on a $12 million revolver and a $22 million term loan. The bank is comfortable with this size of loan given the $40 million equity cushion beneath the senior debt. Oftentimes, $22 million of this loan will be referred to as “senior stretch”, “leveraged loan”, and “air ball”. While these loans may have a first lien on physical collateral, they are underwritten based upon the existing and future cash flows of the enterprise. These are a cost-effective option for companies that have: (i) limited assets but demonstrated cash flow or (ii) a strong collateral base and may be looking for a loan with fewer maintenance requirements than an ABL product.

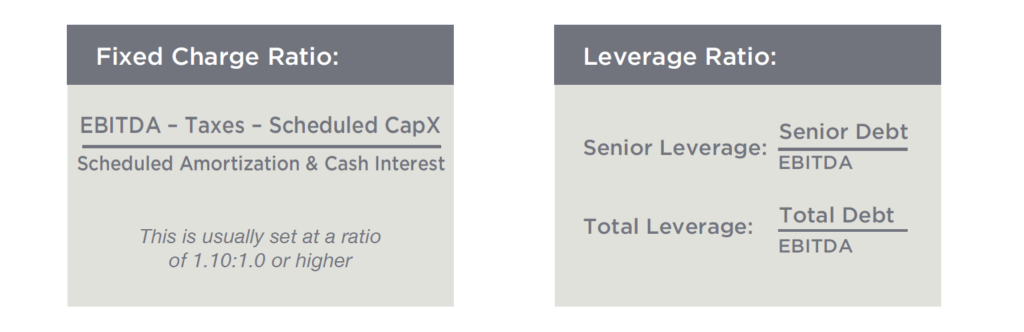

Oftentimes the lender establishes a series of financial covenants which are used to monitor the company’s ability to satisfy the primary loan obligations of interest and scheduled amortization payments. The two most common financial covenants are the Fixed Charge and Leverage covenants (see definitions below).

Since projected cash flow is never certain, a cash flow lender is taking on more risk than an ABL lender and, therefore, will charge a higher interest rate. Regardless of the institution, senior debt is typically the least expensive form of financing as senior debt carries a relatively low risk for the lender; it has first claim on assets. Most senior debt is coupled with a variety of financial covenants, a set repayment schedule, and free cash flow recapture (or a sweep), which further mitigates the risk to the lender by paying down the principal earlier than scheduled. Most regulated commercial banks are underwriting cash flow loans on the basis of collateral, cash flow, and enterprise value, and those who are looking at senior cash flow Term A loans, including the non-bank lenders, are underwriting free cash flow and enterprise value. Regardless of the institution or how they are underwriting, all senior lenders are securing their loans against collateral, which can include fixed assets, real estate, inventory, accounts receivable, a pledge of the company’s stock, and at times, personal shareholder guarantees. Due to financial covenant restrictions, set amortization schedules, and free cash flow recapture features, senior debt is comparatively rigid, but it remains a low-cost solution for companies with relatively steady performance needing to borrow 1.0x to 4.0x EBITDA.

Term B / Second Lien

Term B loans are a type of senior loan that defers the bulk of the principal payment until the end of the term; however, rarely are these loans provided by the same banks that offer ABL Structures, non-ABL Revolvers, or Cash Flow Term A loans. Typically, this loan requires one to two percent amortization with the balance due at maturity. Term B loans will generally mature one year after the senior term loan, and due to the reduced annual payment, these loans carry a higher coupon than senior debt.

Term B, often interchanged with Second Lien, carries a second lien on the company’s secured assets or when alongside ABL structures, a first lien on non-ABL secured collateral and a second lien on ABL collateral. Due to second lien debt having second claim on assets and significantly reduced amortization, the lender holds more risk and pricing will be meaningfully higher than senior debt.

Subordinated Debt

Subordinated debt sits beneath traditional ABL, enterprise value loans, and at times, second lien paper. Mezzanine loans are an interest only, non-amortizing security that have a single principal payment due at maturity, usually 5-7 years after issuance. This security’s return is comprised of a fixed-rate coupon, a portion of which may be structured as payment-in-kind (commonly referred to as “PIK”, deferred, or accruing) interest, or it may have a combination of a fixed coupon and equity appreciation through a warrant or the purchase of common equity. This warrant or equity-enhancement is often used to reduce the size of the coupon, but it still factors into the lender’s risk-adjusted return calculation, which is 200-300 basis points higher than second lien debt.

Sub debt isn’t expensive debt, it’s cheap equity.

Historically, many commercial banks provided subordinated debt, but following the Dodd-Frank legislation, subdebt is primarily provided by private credit investors including insurance companies, standalone mezzanine funds, private equity investors, BDCs, and Small Business Investment Corporation (SBIC) funds. Mezzanine returns will vary depending upon the nature of the primary borrower. For example, subordinated debt when used to support a private equity sponsor in a leveraged buy-out (sponsor mezzanine) will be priced lower than mezzanine structures that are used to support founder and entrepreneur-owned companies (non-sponsored or sponsorless mezzanine). The reason for this is two-fold. First, equity sponsors have the ability and are encouraged or even expected by lenders to invest additional equity if needed to cure a loan default. Secondly, sponsor mezzanine is commonly offered an equity co-investment opportunity, which subsidizes the contractual return on the subordinated debt.

Another key distinction between sponsor mezzanine and non-sponsored mezzanine is that leverage levels can be up to 2.0x higher for sponsor-backed transactions than non-sponsored acquisitions. Both sponsored and non-sponsored mezzanine providers are underwriting the enterprise value of the underlying business and feel most comfortable when there is an equity capitalization of 35-40% sitting beneath total debt. Due to the relative price of subordinated debt, companies traditionally borrow senior debt and even second lien capital before turning their attention to subordinated debt. In the event a company’s collateral base cannot support a second lien note, then a senior and subordinated debt structure are usually a cost-effective solution relative to a unitranche product for non-sponsored loans.

Unitranche

As previously mentioned, capital structures can include multi-tiered debt obligations from two or more institutions, but with unitranche debt, the loan structure is blended to create a single tier and remains senior in nature due to a blanket lien on collateral and stock. Unitranche lending has gained in popularity, particularly in Leveraged Buyouts (LBOs) where non-bank lenders, including publicly traded Business Development Corporations (BDCs), leveraged debt vehicles, credit opportunity funds, CLOs, and hedge funds have entered this segment of the industry. The evolution of the unitranche product has left many of the regulated commercial banks searching for participations and first-out revolvers as way to preserve their revolver and treasury management fee income.

This single tranched loan, displacing both senior and subordinated lenders, will have one blended interest rate and amortization payment, a perceived benefit over working with multiple lenders. Although the issuer will only have to track one lender, there are usually a couple of organizations working behind the scenes. Few unitranche providers have the staff or systems to manage and monitor a revolving line of credit, so a small revolver is placed with a commercial bank of the unitranche provider’s choosing, which is then subject to the Agreement Among Lenders (AAL), a legal document that addresses the various rights of the lenders involved. This document establishes the first-out, last-out terms and principal and interest allocations of the agreement. What the issuer makes up in simplicity is typically forfeit in cost. Historically, the blended rate of a non-sponsored unitranche loan is 150 – 200 basis points higher than the weighted cost had the issuer negotiated the individual debt tranches with different lenders. Furthermore, in the event of default, the unitranche lender votes and acts on behalf of the entire tranche which may be troublesome if the provider is unwilling to work with the issuer and accelerates the maturity of the loan by forcing a sale of the company or an orderly liquidation.

Redeemable Preferred Stock

Redeemable preferred stock is considered equity by those more senior in the capital structure, but this patient instrument is a hybrid of sub-debt and common equity that has repayment priority to common equity. It resembles sub-debt in the sense that it has a set maturity or redemption of the full principal amount of the investment and requires an additional payment to preferred holders which normally comes in the form of a current or compounding dividend. This dividend represents a contractual fixed return representing a meaningful portion of the overall expected return of the security. The Redeemable Preferred Stock resembles equity in the sense that another portion of the investor’s return is realized through equity appreciation by way of a warrant or common equity position also attached to the security. Given the fixed return portion of the security and priority in the capital structure, the Redeemable Preferred Stock does not require a pro-rata ownership of the company as if it were common equity. The mechanics of the redemption will include a maturity and a put option. This put option is a contractual right to sell the warrant or ownership position and requires the issuing company to buy the preferred shares at a predetermined or negotiated value at the prearranged date. The company may negotiate to purchase the preferred shares at an earlier date, particularly if the company believes the value of the shares will increase prior to the investor’s put date. Any repurchase is typically funded with less expensive senior debt assuming there is ample debt capacity at the time of the redemption.

Due to the preferred dividend and in some cases a liquidation preference, redeemable preferred stock is less dilutive than common equity, but unlike a debt security, preferred stock is not tax-deductible.

Convertible Preferred Equity

Convertible preferred shares normally produce returns through dividends that are paid out at a specified constant rate but have limited share appreciation prior to conversion. If a convertible preferred shareholder expects the company’s return on shares of common equity will be greater than the dividend currently being paid out by the preferred share, then the investor will have the ability to convert its shares into common stock. Convertible preferred is commonly found in venture and public company transactions due to the sheer number of short-term liquidity options. For this reason, convertible preferred is rarely found in lower and middle-market capital structures.

Why some companies want their lenders to own equity: Company X financed an acquisition last year with debt and has determined that, in order to add a critical product to its catalog, it needs to spend $8 million for an unscheduled piece of new equipment that will pay for itself in 24 months. To buy it, the company will be required to borrow an incremental $8 million of debt, debt that will undoubtedly place an immediate strain on the company’s cash flow. The company’s lender has no incentive to approve the unscheduled capital expenditure as it will consume financial resources in the short term that would have been used to pay back Company X’s debt; furthermore, this incremental debt only reduces the equity cushion that this group of lenders diligenced as part of their initial underwriting. As a result, the existing lenders may demand to be refinanced or block the company’s $8 million purchase. On the other hand, if that same lender is holding warrants in the company and sees this new line as a meaningful benefit to equity value over the next 36 months, the lender is inclined to approve and possibly even finance the company’s new equipment purchase.

Equity Warrants

Subordinated debt and preferred stock providers, collectively known as junior capital, will be open to the use of warrants as part of the financing structure, particularly if the investor believes that it is taking equity risk, sees the opportunity for stock appreciation, or both. Typically, warrants are attached to subordinated debt or as part of a redeemable preferred stock solution. Company owners can easily reduce their interest rate by offering warrants to the investors or lenders as a component of the overall return. These warrants can be used in place of a contractual return or in addition to it, but the capital provider factors the value of the warrant as part of the annualized target return over the life of the investment. An equity warrant gives the holder the right to buy common shares at a specified and usually insignificant strike price. Warrants typically carry a put, normally 4-7 years, giving the warrant holder the opportunity to exercise their right to sell a set number of shares at a specified time. Equity warrants are attractive to investors as the underlying shares allow their holder to participate in the equity appreciation of the company, which aligns the investor and the shareholders’ interest. This can be particularly compelling in the case of acquisition finance when any number of integration issues may arise, altering the company’s financial projections. If the lender has any ownership stake, there is an incentive to remain focused on the long-term value of the combined entities; whereas, a credit fund that does not have this outlook may exercise its punitive covenants at the first sign of trouble.

Common Equity

Common equity falls at the bottom of the capital structure. Since common equity does not require a cash coupon or scheduled dividend payment, many company owners view common equity as an inexpensive way to raise capital. This is a misperception. Although it is the most patient, common equity is oftentimes the most expensive form of capital. Common equity represents pro rata ownership in equity value created from growth, corresponding cash flow creation, and the repayment of debt. Debt has a fixed cost or return to its lenders, is easily calculated, and should be less than the shareholder returns on common equity. Despite this reality, for shareholders who are debt averse, common equity is sometimes the only option they will consider.

The Common Equity Cost Comparison:

Company A has $6 million of EBITDA and is acquiring Company B with $4 million of EBITDA. Company A has $10 million of debt outstanding on its balance sheet and is paying 6.0x for Company B or $24 million. In total, the combined entity (NewCo) needs $35 million in financing, including $1 million of fees and expenses. NewCo can either (i) issue $35 million of debt with a blended interest rate of 6.5% or (ii) sell a 43.8%]equity stake in the company (8.0x $10 million of pro forma EBITDA ~ $35M investment = 43.8%).

After year one, the company has successfully kept all customers, eliminated $1 million in inefficiencies, and EBITDA is now $11 million. Ignoring taxes and any equity appreciation over the course of the investment, the cost of the debt investment would be $2.28 million (6.5%35,000,000) in year one. If the company chose the equity investment, the pre-tax profit attributable to the investor’s shares would be $4.82 million (43.8%11,000,000) in year one. Additionally, the interest expense from debt is tax-deductible, offering even greater savings.

Selecting the Right Mix of Debt and Equity

The solution primarily depends on each company’s unique situation and outlook. The table below provides further distinction and a side by side comparison of the three main groups of capital available.

After-Tax Cost of Capital

One of the biggest differences between debt and equity occurs when considering the after-tax cost of capital. Interest expenses on debt are tax deductible thus creating a tax shield not offered by equity capital. When considering the cost of financing an acquisition with debt, equity, or a combination, the company must take into account the tax expense reduction in order to get the true price of the debt. Equity will always have a higher cost of capital due to its dilutive nature and inability to reduce taxable income.

Finding the lowest cost of capital should never be the only goal for a company when exploring capital solutions. By striking the optimal balance between cost and functionality, management can build in a cushion for unforeseen issues if the need arises. Of course, there are times where a financing structure that offers the lowest cost of capital is the best choice. However, responsible business owners would be wise to reflect on a few key questions before selecting a form of financing.

For example, what happens to the proposed capital structure if: • A meaningful customer is lost; • The regulatory environment changes; • Raw material prices increase and cannot be passed on to customers; • Interest rates increase; • Minimum wage or cost of labor increases; or • Transportation rates increase? Certain capital structures better prepare a firm to weather these downside factors.

Three financing scenarios: If a $10 million EBITDA company is considering a $40 million commercial bank loan priced at 5.5% pretax with a 5-year straight line amortization schedule, 50% free-cash flow sweeps, and tight financial covenants, once any one of the above downside factors is incorporated, the loan may be unsuitable. Knowing this, the company might consider any one of the following, more flexible, alternatives instead:

$40 million unitranche loan amortizing at 2-5% with 50% free-cash flow sweeps priced at 7.5% pretax;

$30 million term loan with 10-year straight line amortization priced at 5.5% which is sitting ahead of $10 million of non-amortizing 13.5% subordinated debt (blended cost is 7.5% pretax); or

$20 million revolver, drawn at 50%, and priced at 3.5%, paired with $10 million of 10-year amortizing term debt priced at 5.5% and $20 million of preferred stock (blended pricing is at 10.75% pretax)

The initial structure was priced very low but left little room for the company to deviate from its forecast. Scenarios 1 & 2 offer comparable pricing, and the financial covenants offer greater flexibility than the initial structure. Although Scenario 3 has a higher blended cost of capital, the company will have very low scheduled debt payments, which creates an inherent flexibility should an exogenous disruption occur. By offering a very high margin of error for the company, Scenario 3 is the most conservative option.

Ultimately, responsible acquisition financing must balance market based pricing and structure with management’s confidence in their ability to deliver on stress-tested financial projections.

Selecting a Capital Provider

Though selecting the right capital provider has a large effect on the success of an acquisition, each capital source has unique characteristics.

When deciding on the source of the capital to finance an acquisition, Cyprium has found three attributes to be highly important:

Is this provider and its investment team established? During the Great Recession, many specialty credit funds were dismantled, their portfolios sold off, and the investment teams sidelined. This resulted in the underlying issuer working with new portfolio and relationship managers, and in some cases, through counsel. Although there will be many compelling term sheets worth considering, an issuer should take the lenders’ history into consideration and ask for references if none are provided.

Does this group think like a lender or a shareholder? There are two types of capital providers: those who think like lenders and those who think like shareholders. Lenders have limited ability and appetite to take risk. Loans are generally highly structured, fully collateralized, and amortize or sweep cash as quickly as possible to reduce risk even further. Diligence and company analysis may be limited to risk mitigation by means of collateral and cash flow recapture. The real challenge facing a business owner is finding a capital provider that genuinely wants to learn about the company. The investor-minded capital provider asks insightful questions about how the company works, the value of its products and services, operational challenges in the business model, and the competitive landscape. It may even attempt to provide the company with potential solutions to the challenges it faces. Over the course of any relationship, the impact this degree of interest can have on the working relationship between the capital provider and the company will be significant. At the first sign of trouble, a lender will get nervous and begin thinking about how to recover principal. The investor-minded capital provider will patiently work with management to find a solution.

Are they experienced in my industry and with this type of investment? Regardless of whether the capital source is a commercial bank or private credit fund, it is important that any provider possess demonstrated experience with both the type of transaction proposed and the industry of focus. Financing an acquisition can be a complicated process, so having a firm that has been through the process before helps improve the chances for a successful transaction, both at close and over the course of the loan and/or investment.

Third Parties, Diligence, Fees & Timeline

Depending on the type of financing that a company selects, there can be any number of third parties involved with due diligence work streams.

The following costs and timeline assume that a company’s records are in order: Asset Appraisal Firm: Subject to the type of financing that a company is pursuing, secured lenders will require an asset appraisal, which will cost between $15,000 and $25,000. Time to complete: 3-5 days onsite; the CFO should individually dedicate 8-12 hours for Q&A if all the paperwork and systems are current. Total time for a final report: 10 days.

Background Checks: Every capital provider will want to complete background checks on the shareholders and key members of management. As a result of this, it is best to disclose all items of concern with the investors long before those items surface during a background check. A standard background check will cost between $5,000 and $15,000 in total, and typically, one report will suffice for all capital providers assuming they all agree on the provider before the report is commissioned. Total time for a final report: 2 weeks.

Environmental: If the parent company or the acquisition target owns real estate, it is prudent to complete a Phase I environmental site assessment. These can range from $2,000 to $50,000 depending upon the level of complexity. Total time for a final report: 2-6 weeks.

Insurance: A cursory insurance review will be completed on both the acquiror and the acquisition target. Typically, there is little to no cost associated with these reports as most brokers will offer a comprehensive analysis of plans and will offer cost-effective alternative policies. Total time for a final report: 1-2 weeks.

Legal: With multiple entities at play, there will be significant legal fees. For a relatively efficient process with few complications, assume up to $150,000 per legal team; there will be one legal team for every buyer, seller, and third-party capital provider. Total time for legal: 3-4 weeks.

Quality of Earnings/Accounting: Due to the sheer magnitude of capital options alone, identifying investors and sifting through debt proposals can monopolize a CFO’s time; furthermore, many CFOs become bogged down in diligence, either responding to diligence request lists from capital providers, or performing due diligence on the acquisition target. All of this is aside from overseeing day-to-day financial planning and analysis, tracking company performance, and closing monthly financials. Concurrent with the negotiation of a letter of intent (LOI) on the acquisition target, it may be prudent for the buyer to have a thorough Quality of Earnings analysis done on itself in order to help ease the burden during the financing process and pre-close diligence.

The Quality of Earnings report on the buyer and the seller will each cost approximately $50,000 to $125,000 depending upon the scope of the project and complexities. Aside from compiling and fulfilling the data request, the CFO of each company should anticipate spending at least 3-4 days with the diligence team on site This is in addition to the amount of time the CFO and its staff will spend in fulfilling diligence requests. Total time for a final report: 3-5 weeks.

Additional Closing Fees: Most capital providers will negotiate anywhere from 50 – 200 basis points at close on the total investment each provider is making in the company. This fee will be paid for by the company and will be in addition to all out-of-pocket legal, financial, diligence, and other miscellaneous fees covered.

Timeline: While the timeline for a transaction will vary, 45-60 days is standard once the buyer has negotiated a LOI with the seller assuming the seller and buyer are organized and have their third parties selected and scheduled to begin.

IN SUMMARY

Acquisition financing can be a complicated process, but it does not need to be. Seeking the right advice and creating the right plan from the beginning can greatly reduce the challenges that come with financing an acquisition.

Specifically, when making a financing decision, business owners should:

Know the different forms of capital available for financing;

Contact capital providers early in the process and budget minimum of 60 days to be safe;

Decide what capital structure would be best;

Choose the right capital provider for the transaction at hand taking into consideration both the present and future;

Execute what is hopefully a smooth transaction that works out well for all parties involved;

Make sure the right structure is in place both financially and managerially to assure the integration of the newly acquired company is successful.”

About Cyprium Partners

Cyprium Partners is a private investment firm that makes non-control investments in profitable middle-market companies, allowing company owners and their management teams to retain controlling interest in their businesses.

For over 20 years, the Cyprium team has been investing alongside founders and entrepreneurs to support growth, shareholder dividends, minority recapitalizations, ESOPs, debt reduction and strategic acquisitions, a handful of which are offered as examples below.

Cyprium can provide any combination of subordinated debt, preferred stock, or minority common equity, offering flexibility and increasing certainty of close.

With offices in Cleveland and Chicago, the firm invests $10 million to $60 million per transaction in U.S. and Canadian companies that have $8 million or more of EBITDA. Investors include pension funds, insurance companies, financial institutions, funds-of-funds, family offices and entrepreneurs who the firm has backed in previous investments. Since 1998, the firm has invested in excess of $1.6 billion in over 90 platform investments. Learn more at www.cyprium.com.

For questions regarding Cyprium’s experience or to discuss new investment opportunities, please contact: